Elray Resources, Inc. (OTC: ELRA)

$ 0.0035 ▲ 0.0026 (288.89%)

Volume: 315,059,116

Elray Resources is up sharply in its most recent session, but likely for the wrong reason. They canceled a reverse split While many investors may see this as a great win, it was put on the table. It may have been canceled, but we all would suspect the shareholder rage after it was announced. The company says “This decision was reached as a result of positive opportunities and achievements by the company in recent weeks.”

The chat room spin even Sunday is mostly positive:

“One of the main reasons a CEO will cancel a split that i have found and seen many times, usually they have a big deal or contract they have landed… ELRA dropped for only one reason over the past couple months. Asher and announced R/S. They are both gone. This will be up in the pennies real soon again… MARK IT.” (Some random Ihugger)

Of course you can never truly trust an Ihub chat room as they are so managed.

The company showed its cards. They want to do a reverse split. The insiders have little to lose unless it causes a huge uproar and legal issues. Today they have changed their opinion on it, and for now it is delayed.

I don’t see an upside here.

PROFIT? WHERE?

I really find it repugnant that the company would use this all caps header in a recent press release:

“PROFITABLE GROWTH OVER THE LONG TERM”

How can they even use the word “profitable” in a release? They are going from nothing in revenue to some revenue. That is growth. If I sell dreams written on a piece of paper as my business and I sell none in one quarter and three in the next quarter, there is growth in my sales of dreams. It doesn’t mean that I am going to continue into profitability. Especially if my accumulated deficit during the development stage was a whopping $17,633,716.

You’ve got to ask yourself if you are serious about this one, were they even trying to really do anything if they burned through a development stage deficit of $17,633,716?

THE INTANGIBLES ARE WORTH HOW MUCH?

I loved this entry on their filings:

Intangible assets: $2,986,112

What are these intangible assets?

“Intangible Assets: Intangible assets consist of expenditures for domain names and certain intellectual properties acquired for an online horse racing product the Company is developing. The intangible assets are recorded at cost and amortized over estimated useful life of 3 years.”

They have got to be joking. Let’s look at the domains to start with. I assume the only operating entity is where the real value is, right?

SIMVRACING.COM DOMAIN HAS NO TRAFFIC SHOWING WITH QUANTCAST OR ALEXA:

That domain was registered on May 4th of THIS YEAR:

WHOIS information for simvracing.com:

Domain Name: simvracing.com

Created On: 04-May-2014

So if I bought this domain on May 3rd, would I have been able to flip it for millions the next day? Is it that “valuable?” I don’t think so!

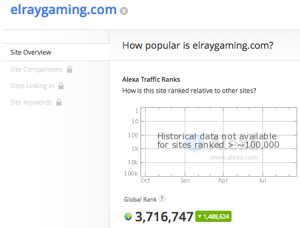

ELRAYGAMING.COM IS WAY DOWN IN ALEXA, NOT SHOWING TRAFFIC ON QUANTCAST:

Their main domain gets almost no traffic, but maybe it is the one worth millions?

Domain Name: ELRAYGAMING.COM

Updated Date: 2014-01-30

Creation Date: 2011-02-14

Let’s assume that their intagables are truly worth $2,986,112, then that means the remainder of the intangibles – described as “… and certain intellectual properties acquired for an online horse racing product the Company is developing” are worth about $2,985,000.

Investors drinking the Kool-aid may answer with this:

The filing says: “The intangible assets are recorded at cost and amortized over estimated useful life of 3 years.”

The easy answer is that after these years of operations and burning through a development stage deficit of $17,633,716, I am sure they can easily apply close to $3 million of that burn to these intellectual properties. I am sure they were not using the development stage deficit on corporate retreats and first class travel. They had to spend it on something business related. Hence, IP.

What’s this stock worth?

When a company like this suggests it needs a reverse split and it has three classes of preferred, you can easily expect a 95% decrease in the value of the common shares over a year. Yes, they pulled it back. Wow. Amazing.

Basically I value the common shares at nearly nothing. I see no real value when the company has burned through cash at astonishing rates with little to nothing to show for it – AND – they showed a serious interest in a reverse split. They have so many ways to protect the Preferred shareholders from any price the common shares may hit that there is no reason to believe that they will continue to look out for the common shareholders in the future.

Do you believe their reason for pulling back the reverse split just days out? Let’s look at why companies would pull that back. These include:

- A result of positive opportunities and achievements by the company in recent weeks. <Their stated reason

- Investor outrage

- Possible investor legal action

- Regulators – or the fear of regulators

- Suddenly you see the light and you realize that these shares are going to be worth so much more, so why undermine the holdings of the common share holders? Stop it while we still can!

- Differences of opinions internally with the insiders

- God spoke and told them not to do it

Good luck to all in ELRA!